The number of life insurers used by financial advisers has fallen to its lowest level in three years yet more than a quarter of advisers are looking to establish a relationship with a new insurer in the next 12 months, according to Investment Trends.

Data released as part of the research group’s ninth annual Planner Risk Report has revealed that advisers providing life insurance advice are only using an average of 3.6 life insurers, down from 3.8 in 2016 and 3.9 in 2015 – the highest level recorded in the history of the report.

The report also found that 47% of advisers stopped using at least one insurer in 2016, a minor increase on the 2015 figure of 45%, but a significant increase on the 2014 figure when only 35% of advisers said they stopped using at least one insurer.

Investment Trends found that while advisers were ending a relationship with an insurer they were engaging in new relationships with other insurers but the take-up rate of the latter had fallen in recent years.

Investment Trends found that while advisers were ending a relationship with an insurer they were engaging in new relationships with other insurers but the take-up rate of the latter had fallen in recent years.

According to the research group, in 2013 advisers stopped dealing with 0.8 insurers on average but engaged with 1.1 other insurers. This pattern continued into 2014, where advisers stopped using an average of 0.6 insurers but engaged with 0.9 other insurers.

This trend, however, has reversed during 2015 and 2016 with advisers no longer using an average of 0.6 insurers and only engaging with 0.4 insurers instead.

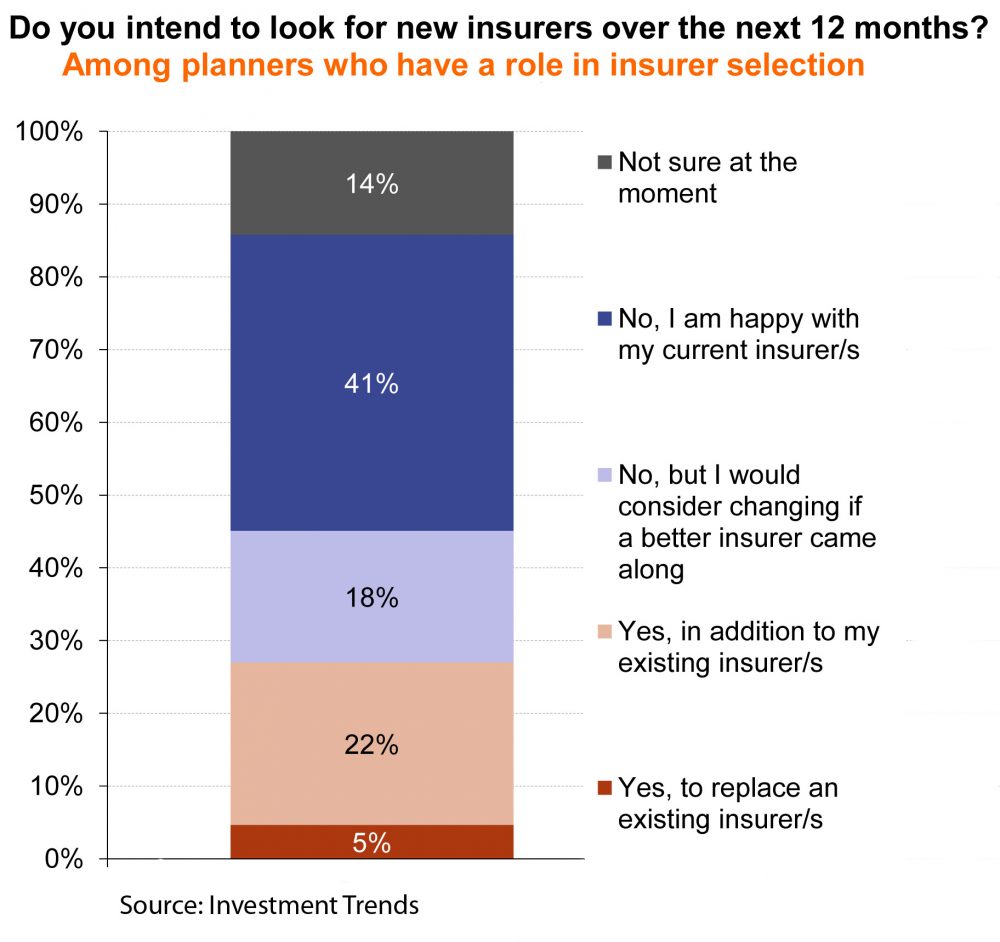

Investment Trends also found that high switching levels were likely to continue with 27% of advisers who had a role in selecting a life insurer stating they would establish a relationship with a new insurer to replace an existing insurer or to add to their list of current insurers.

A further 18% of advisers said they were not currently considering a change but would be open to doing so if they found a better insurer.

Underwriting processes ranked highly among reasons why advisers remained or left an insurer with good underwriting processes named as the leading reason advisers chose to use a particular insurer for the third consecutive year.

This was followed by product features and policy definitions while high premiums and poor underwriting practices ranked highly among reason as to why an adviser stopped using an insurer in the last 12 months.

Hold the Press! Risk advisers re-assess loyalty to insurers. That was odds on, after being speared by the FSC and LIF, in the name ( apparently ) of consumer protection.

Its not over folks. One insures is folding super products which pay a minute trail, folding them into new products which don’t. The trail might not be worth all the Opt In rubbish, but it might have been nice to be consulted.

One Path, up for sale, notified advisers last week that post 1 Jan, new business risk would NOT pay commission on CPI increases.

They can rot on whichever vine they end up on. Why would any business man adviser write new business for them post LIF.

I assume you mean they would not pay new business commission. They are still paying trail (like many/most other insurers do)?

As I understand the issue, this insurer will pay no new business commission on the CPI INCREASES which increase the premiums.

New business commission will be payable only on advised increases. I wonder, if the advised increase occurs just before the CPI increase is due( policy anniversary), will the adviser have his new business commission reduced by the element for the CPI increase, if it had happened.

Trail will increase, but that’s not the point.

Not all insurers pay new business on CPI increases, but most do. This particular commission is the real value for advisers in maintaining a book.

BTW, having put up risk premiums after Xmas, One Path announced today they were rising again soon

Its simple. The old jalopy is being prepped for sale. A few bananas in the diff.

Given the insurers complete lack of any loyalty to advisers and their ongoing viability it should come as no surprise why we would be disloyal…

Adviser loyalty has completely gone just as the insurers loyalty to advisers went with the con job that was the LIF. Most of us are probably sick of getting the “we want to support you through the LIF emails”.

I think most advisers are ready for the LIF and the new education standards. Many will stop writing new business and sit on trails. Many will start offering other services and many will retire early instead of completing education that may only see them stay in the industry a few years more.

Its the insurers who are not ready for the LIF. They will be fighting for a share of a much smaller new business pot but they are not ready to cut their excessive pays and excessive staff numbers but that is what they will have to do. Or they can keep increasing premiums and making the problem worse.

What loyalty?? You reap what you sow FSC.

There used to be adviser loyalty before we and the Australian public all got screwed by the FSC (insurance companies & banks).

If insurance companies had wanted to support us they would have fought against LIF not push LIF through as quick as they could. Disgraceful behaviour and extremely disappointing.

After almost 30 years providing insurance advice (most of which has been fun) it has become a lot more unenjoyable and stressful business to be in. Hopefully the insurance company management bonuses will be cut dramatically and they (like advisers) also feel some financial pain.

Comments are closed.