MLC Life Insurance has released a new Supplementary Product Disclosure Statement for its MLC Insurance series, which it says includes a range of significant enhancements to its definitions and policy terms.

Detailed in a summary released to advisers last week, and taking effect from 16 April 2019, key changes include:

Detailed in a summary released to advisers last week, and taking effect from 16 April 2019, key changes include:

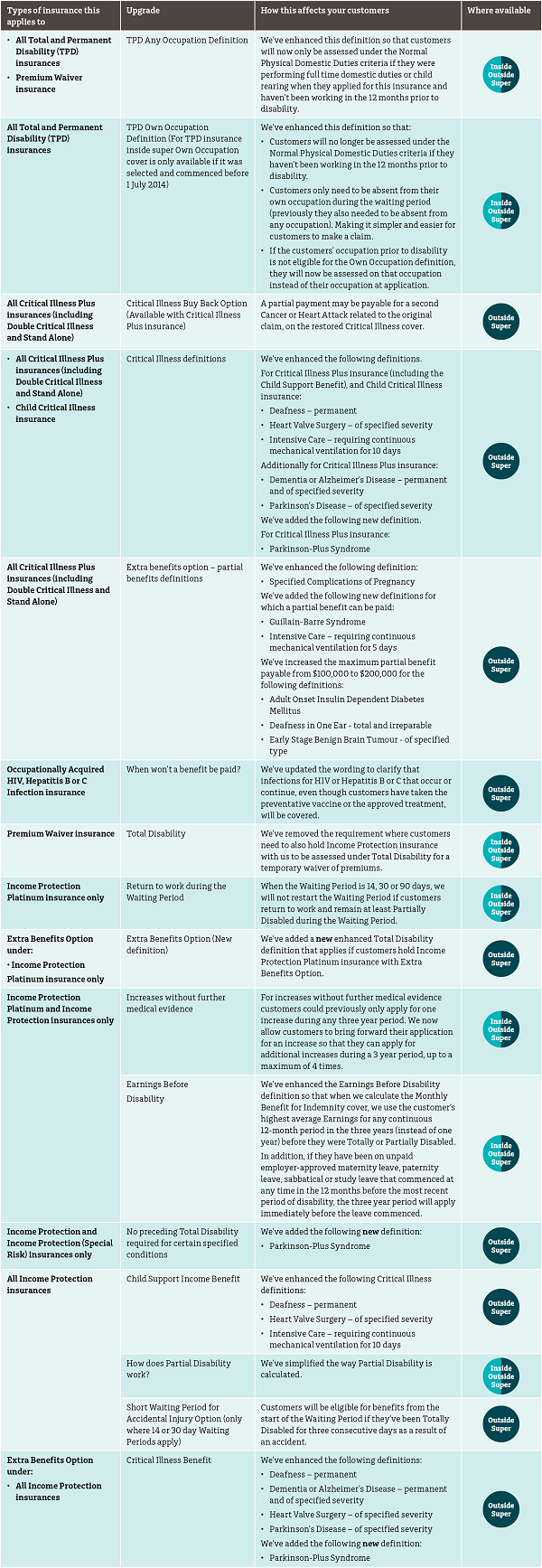

TPD Cover

TPD Any Occupation

The insurer says it has enhanced its TPD Any Occupation definition so that customers will now only be assessed under its Normal Physical Domestic Duties criteria if they were performing full time domestic duties or child rearing when they applied for insurance and haven’t been working in the 12 months prior to disability.

TPD Own Occupation

Under Own Occupation TPD, the insurer notes it has enhanced its definition so that:

- Customers will no longer be assessed under its Normal Physical Domestic Duties criteria if they haven’t been working in the 12 months prior to disability

- Customers only need to be absent from their own occupation during the waiting period, whereas previously they also needed to be absent from any occupation

- If the customer’s occupation prior to disability is not eligible for the Own Occupation definition, they will now be assessed on that occupation instead of their occupation at application

Trauma Cover

For all policy owners holding the Critical Illness Buy Back Option within MLC Insurance’s Critical Illness Plus product, a partial payment may now be payable for a second Cancer or Heart Attack related to the original claim on the restored Critical Illness cover.

Click here to access a summary document provided to advisers, which contains details of additional trauma and income protection enhancements and other changes applicable to MLC Insurance, MLC Insurance (Super) and MLC Insurance (Wrap or SMSF) policies.

…And click here to access the new combined SPDS/PDS for the MLC Insurance range of products.

The insurer also confirms these changes are applicable for both new and existing policy holders.