New research suggests many Australians would prefer to pay an upfront fee for life insurance advice if this translated into lower premiums over the lifetime of the policy. Reflecting on this finding, CoreData’s Kristen Turnbull asks the question: are consumers really prepared to put their money where their mouth is?

The age-old debate about fees versus commissions has become a distant memory in the financial planning industry, with advisers no longer able to charge commissions relating to investments for new or existing clients.

However, in the risk advice world the debate rages on, and new research recently released by Metlife has added fuel to the fire. The research suggests most Australians (78%) with life insurance purchased through an adviser would prefer to pay an upfront fee for advice – provided it meant lower premiums over the lifetime of the policy.

This caveat is important, because they’re understandably only willing to make this change in exchange for some level of personal benefit, namely a reduction in premiums.

Disclaimer: I’m not a fan of the commission structure in general. I think it lacks transparency, and essentially devalues the important role an adviser plays in the mind of the consumer.

If you’re putting your hand in your pocket, you know exactly what you’re paying and you’re making a conscious choice that the product or service is worth the fee you’re being charged. Ostensibly, you perceive value in what you’re buying. If you’re not paying a fee directly, then you’re no longer making that conscious choice.

This assumption is backed up by CoreData’s research, which suggests only half of consumers (51.6%) with life insurance cover outside super know how much this costs them each year.

But while shifting to fee-only risk advice sounds like the best way forward in the interest of full transparency, we all know insurance is sold, not bought. In the life insurance sector, the simple inclusion of that trail commission removes a key barrier for consumers in taking up life insurance in the first place; they simply don’t want to pay for it.

One of the interesting things about human behaviour is that our perceptions of what we want, or need, don’t always match the reality. In behavioural science, this is known as cognitive dissonance.

Cognitive dissonance, in essence, is the gap between what you say and what you do. It’s when your words, thoughts or actions contradict your beliefs.

Saying you’d prefer to pay a fee is one thing; actually paying it is a different thing altogether.

Early indications suggest that advisers tend to agree. A poll by Riskinfo asking advisers to estimate what proportion of their clients would be prepared to pay a fee for their life insurance advice found most (68%) put this figure at less than 20%.

As MetlLife acknowledges in its paper Understanding the Adviser-Client Relationship Report 2019, many Australians (72%) think that removing commissions will exacerbate the underinsurance gap.

While the reason for this wasn’t qualified by the research, the paper suggests it may be that consumers see such a move leading to higher up-front fees, causing people to choose lower levels of cover.

I would surmise that it could also be because they realise that there’s no such thing as a free lunch. The higher upfront fee that will need to be charged by advisers to recoup the loss of commissions would be unpalatable to many, and hence fewer people will actually take out the policy – even if the potential to have those commissions rebated back to them makes the policy cheaper over the longer term.

But charging a higher upfront fee is also problematic for advisers, who are already being squeezed under the LIF remuneration rules.

From 1 January 2020, upfront commissions are capped at 66% of the premium in the first year with a 22% trailing commission.

Research conducted by CoreData in mid-2019, when the upfront commission remained higher at 77%, revealed four in five (79.5%) advisers had experienced a reduction in practice revenue as a result of the reduction in upfront commissions, with more than one in five (21.8%) experiencing revenue loss of more than 25%.

Perhaps more concerningly from an affordability and underinsurance perspective, is the fact that nearly two thirds (65.0%) of advisers say LIF has caused them to place greater focus on high net worth clients, creating a potential risk advice gap among middle Australia.

The Law of Unintended Consequences suggests there are three types of unintended consequences:

- Unexpected benefits

- Unexpected drawbacks

- Perverse results

While exacerbation of the underinsurance problem, lack of affordability for the mass market and a reduction in practice profitability for risk specialists can be classified as unexpected drawbacks at best, and perverse results at worst, there is one benefit – not unexpected – that would likely come from the removal of commissions on risk advice. That is, an increase in consumer trust.

Trust in the financial services industry at large took a hammering during and post Banking Royal Commission, as the true extent of the misconduct was revealed.

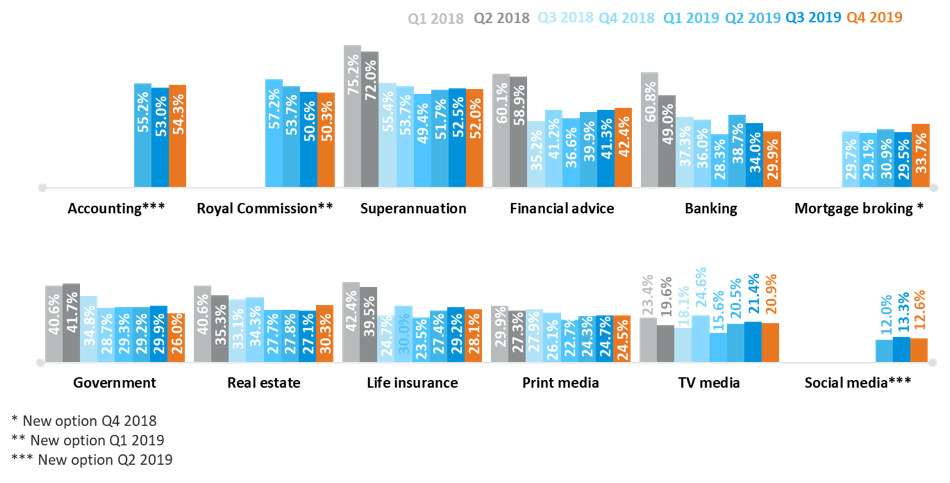

CoreData Quarterly Trust Survey

Towards the end of 2019, trust was yet to recover to pre-Commission levels across most areas of the industry. In the life insurance sector in Q4, trust was sitting at just 28.1% – below banking (29.9%), financial advice (42.4%), superannuation (52.0%) and accounting (54.3%).

Towards the end of 2019, trust was yet to recover to pre-Commission levels across most areas of the industry. In the life insurance sector in Q4, trust was sitting at just 28.1% – below banking (29.9%), financial advice (42.4%), superannuation (52.0%) and accounting (54.3%).

In other words, less than one in three Australians rate their level of trust in the life insurance sector at least six out of 10, while for financial planning only two in five trust the sector, in line with the number of Australians who tend to seek financial advice.

A rebound in consumer trust would be a welcome development for both parts of the sector, but if this comes at the expense of advice access and affordability, then nobody wins.

Kristen Turnbull is Director, CoreData WA and responsible for life insurance research within the CoreData Group