Life insurance commissions should remain as a valid form of remuneration for advisers and the prevailing hybrid commission model should revert to 80/20…

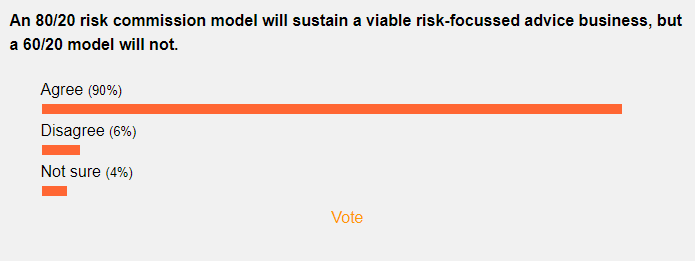

Riskinfo’s current poll results strongly support the contention that an 80/20 commission model will sustain a viable risk-focussed advice business, but a 60/20 model will not.

While we never claim scientific rigour around our poll results, we’ve been doing this for long enough to be confident that the results below reflect a general industry sentiment that reversion to an 80/20 hybrid commission model will indeed make all the difference in sustaining risk-focussed financial advisers.

‘All the difference’ means that at 80/20 a high proportion of risk-specialist advisers will have the opportunity to remain focussed on their passion – life insurance advice solutions – while at the same time retaining a fighting chance to build a viable and, dare we say it, financially successful business.

‘All the difference’ means that at 80/20 a high proportion of risk-specialist advisers will have the opportunity to remain focussed on their passion – life insurance advice solutions – while at the same time retaining a fighting chance to build a viable and, dare we say it, financially successful business.

Financial advisers have been shunted from pillar to post in recent years by an ongoing regulatory reform agenda which has included the Future of Financial Advice reforms, the introduction of minimum education standards and an adviser exam via FASEA, the Life Insurance Framework reforms and other measures driven by recommendations made in the final report of the Financial Services Royal Commission.

…unintended consequences …are actually making it harder for consumers to access the quality advice that so many desperately need

It seems, though, that risk-focussed advisers have borne the brunt of these measures – reforms that have been motivated by a genuine desire to improve consumer protections, but where the unintended consequences accompanying their implementation are actually making it harder for consumers to access the quality advice that so many desperately need. That is, the cost of life insurance advice continues to rise and the number of advisers continues to fall.

Riskinfo supports the continuation of risk commissions and the ability for any financial adviser to have the option to be remunerated via commission when placing risk business. Advisers can also charge fees for their life insurance advice (although experience suggests this is not a commercially viable option), or the cost of the life insurance advice component absorbed into the investment fees and charges. The point, however, is that the adviser and importantly, their client, should at least have that choice.

We appreciate the contention that all commission-based remuneration is conflicted. Even when there exists a single commission model common to all product manufacturers – where there is no opportunity for advisers to access better commission arrangements from individual providers – there remains the matter of the amount of cover being placed: the higher the cover, the higher the commission.

The entire industry now operates, however, under an environment in which the client’s best interests are mandated by law, and with high upfront commissions now banned and minimum education standards required to be met by all advisers, it is time for the Government, the regulator and the consumer lobby to take a step back and allow risk advisers to get on with the job.

There are two significant assumptions we’re making in this call to return to 80/20 – firstly, that the outcome of the 2021 ASIC review of the quality of life insurance advice will be such as to allow ASIC to recommend to the Government that risk commissions should remain as a valid form of remuneration, and for the Government to accept that recommendation.

…the 60/20 commission cap isn’t commercially viable

As we’ve noted in our poll commentary, however, retaining risk commissions at their current cap of 60% in the first year and 20% ongoing is not a formula which will allow most risk-focussed advice businesses to continue operating. The overwhelming message we receive from advisers is that the 60/20 commission cap isn’t commercially viable.

According to Riskinfo’s adviser audience, however, 80/20 works. This leads us to our second significant assumption, namely that existing laws on commission caps can be rolled back. But that is exactly what we’re advocating.

Post a favourable outcome of the 2021 ASIC review of the quality of life insurance advice (assumption number one), we advocate that the Government should amend the Life Insurance Framework reform legislation to allow advisers a realistic opportunity to create a viable business based around life insurance advice – advice that is and will continue to be in the best interests of both the current and future clients they serve.

The ability for an adviser to access 80% commission in the first year will not adversely affect the quality of life insurance advice…

The ability for an adviser to access 80% commission in the first year will not adversely affect the quality of life insurance advice. In fact, it may well improve the overall standard, because an 80/20 model will allow more life insurance specialists to continue their chosen vocation. What’s the point of maintaining a 60/20 commission mandate when there will be few, if any, risk specialists left to advise? If this happens, holistic or generalist advisers, who aren’t steeped in the nuances and complexities of life insurance advice will likely deliver a lower overall quality of advice than the specialists who won’t exist in any meaningful numbers should the present commission cap arrangement be retained.

We contend:

- Banning risk commissions or even retaining them at 60/20 will lead to an unintended consequence of significantly fewer Australians accessing quality life insurance advice.

- Amending the law to mandate an 80/20 hybrid commission model will not have an adverse impact on the quality of life insurance advice and may well improve it.

We assert that the move to a 60/20 commission cap under the Life Insurance Framework reforms was at least in part an arbitrary number, based on the symmetry of 60% upfront commission being exactly half of what it used to be. In reality, though, the 60/20 model is proving unviable – uncommercial – for thousands of dedicated advisers who have their clients’ best interests at the heart of their value proposition, and we challenge the Government to reconsider.

We see an 80/20 hybrid commission model as a win for all advisers, and for risk specialist advisers in particular. The consumer will also be a big winner if the 80/20 model is re-introduced, as this move will address the unintended consequences brought about by the LIF remuneration reforms and will give more Australians a greater opportunity to access quality life insurance advice – advice that makes such a positive difference in the lives of so many.

80/20 works.

Peter Sobels is Riskinfo’s Publisher and Managing Editor…

Peter Sobels is Riskinfo’s Publisher and Managing Editor…

Great article Peter and a step towards a brighter future if the Government listens and acts.

All Advisers want viable and profitable Life Insurance Companies, so they are able to grow and pay claims.

What holds them back is the Life Insurance Framework ( LIF ) Regulatory regime, that has slammed the breaks on their ability to grow their books and restrictions of trade on all advisers, to the point that it is not viable to write new Business.

No Business can survive, especially Life Insurers with growing claims and reducing revenues.

Paying a higher commission is not just a single issue that will fix the Industry, though it will help advice practices pay their bills.

The Government must realise, that unless they start listening and acting on the clear and concise advice we have been giving to them, that all the Regulator input, counts for ZERO.

It does not matter what ASIC, or APRA, or Treasury think needs to be done. They do not provide the advice and services, we the Advisers do.

We will decide the direction the Industry goes, no-one else, as ultimately, if these entities continue to not listen and do not change the unworkable LIF and FASEA maze of complexity for negative return, then we simply walk away.

If this occurs, then everything the Government and the Regulators have spoken about and put in writing on a continual basis, will be shown to be false, which will leave them open to further action.

A well written article Peter – it sets out the issue with clarity. What RiskInfo contends is indeed a first step in the right direction. However, as Jeremy Wright has alluded to, the FASEA impositions must be addressed, and as has been said in previous comments by other advisers, this 2 year clawback also must be addressed. One question Peter – is RiskInfo going to put forward some kind of recommendation to ASIC, and/or advise them the results of your surveys?

Since 1995, I have been writing business on the old hybrid model and 80/20 is as close to that as you can get. Enough revenue in year one to write the business and good revenue in following years that enable you to spend quality time with your clients providing ongoing service, especially at claims time. It would make an Old Fella very happy to see this level of remuneration return. Although, to be honest, red tape makes this harder, no matter what the revenue model.

Nothing like experience to make your point and I think it will be a solution to the overreach reaction by the regulator that has seen the current dramatic drop in new business sales and the significant increase in lapse rates resulting from product repricing.

Comments are closed.