Riskinfo’s Story of the Week offers advisers the opportunity to deliver their initial verdict on the new range of IP products launched into the market. We’ll be reporting the results in the coming week, but you can take a sneak peak of the outcome so far, which appears to suggest there’s still a tough road ahead for most advisers when engaging with their clients about the value of income protection insurance…

- Agree (72%)

- Too early to tell (15%)

- Disagree (13%)

With the dust settling on the launch of the new IP product offers across the industry, we’re keen to get your initial take on how this will impact your advice proposition.

The new income protection insurance product offers reflect the dictates inherent in APRA’s IP intervention, and contain more restricted definitions in a number of areas, the sum total of which is intended to deliver a more sustainable outcome for both the product manufacturer and the product consumer (see: APRA Cracks Whip…).

But will the less expansive product offers curb the effectiveness of your income protection conversations with your clients? What are your first impressions?

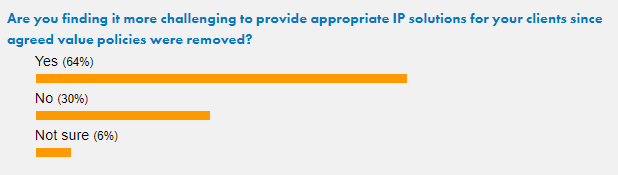

We’ve already had a taste of what advisers think, when around two thirds said the removal of Agreed Value IP products after 31 March 2020 made it more problematic to provide appropriate solutions for their clients:

Back then, one adviser predicted the 1 October 2021 changes would represent a ‘disaster in the making’, especially for self-employed clients (see: Advisers Find Challenges in Providing IP Solutions).

Back then, one adviser predicted the 1 October 2021 changes would represent a ‘disaster in the making’, especially for self-employed clients (see: Advisers Find Challenges in Providing IP Solutions).

Is this your view? Is this new set of IP product offers a ‘disaster in the making’ for consumers? Or can you work with this new ‘IP normal’? Will it be ‘business as usual’ for you when it comes to IP? Or has the value landscape now changed to such an extent to have you reflecting on how you approach this most critical conversation with your clients?

Tell us what you think and we’ll resume the conversation next week…

The removal of the agreed value option is obscene. Sorry, can’t think of a more polite term to use. The solid contractual definitions that formed the core of good IP policies are absent. From what I’ve seen of these ‘new’ IP policies they resemble something you’d buy over the internet from some dodgy carrier. Oh, wait . . . hmmm. Yes, robo-advice will be coming to the fore over the next few years – it will simply HAVE to as there’ll be no experienced advisers left, certainly not in the risk space. So, my preliminary summation of these new-age IP policies is that they are NOT worth the paper they are NOT written on.

This is the beginning of the end for life companies in Australia. You’ll see consolidations, take-overs and life offices withdrawing from Australia like never witnessed before. All because the life companies did not support their life blood – the experienced advisers, when it counted – i.e responsibility periods, commissions et al. They should have championed our cause when they had the chance – things WOULD be different now. Far too late now, sadly. Events and processes are in place now that cannot and/or will not be changed.

Comments are closed.