- Agree (61%)

- Disagree (32%)

- Not sure (8%)

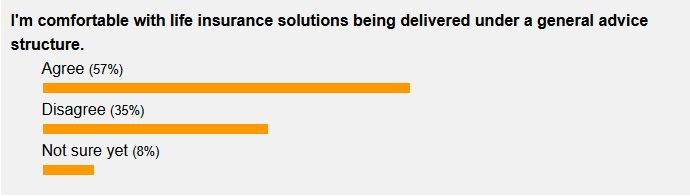

The results from our latest poll suggest the majority of the adviser community has consolidated its tacit support for general advice playing a role in delivering life insurance solutions for Australian consumers.

As we go to press, six in ten (59%) of those taking this poll say they’re comfortable with life insurance solutions being delivered under a general advice framework. One in three (33%) disagree with this proposition, however, with 8% yet to make up their mind.

This conversation flows from recent research indicating 4,000+ advisers who don’t meet the experienced practitioner requirements are yet to formalise their minimum educational qualifications required before year’s end.

It also continues the debate from earlier this year when we asked you the same question, and which delivered a similar result:

This current poll result has been welcomed by Australian Advisory’s Operations Manager, Nathan Kassouah, who says the general advice proposition is gaining ground as what he describes to be a flexible, compliant, and scalable alternative that complements traditional full advice:

“There is growing momentum behind the general advice model, but we still see a significant gap in understanding—particularly among advisers who are unsure or opposed to it,” says Kassouah (see: Renewed Call for Advisers to Consider General Advice Pathway).

He stresses that general advice is not a diluted version of personal advice, but a distinct service model focused on educating and empowering clients:

“General Advice is about educating clients on their insurance options to help them make informed decisions. This model runs in parallel with full advice, serving different client segments within the market.”

Our poll remains open for another week and we welcome your views on an issue which continues to polarise adviser opinion…

Where it all went wrong with the Government, the Regulators, the vested interest groups, was that rules and regulations were set up with NIL, or at best, little consideration for HOW the Life Insurance sector works in the real world.

People seek out and are prepared to pay for Investment / Retirement advice because they see the need and are genuinely interested, whereas Life / Disability Insurance is not a priority, it is a scary and confusing maze of illegible words and is mostly put into the too hard basket, or let's look at this 'later,' category.

So, in their infinite wisdom, or lack thereof, the rule makers decided to put risk advisers into the same basket as Investment / Retirement Planning Advisers and created a TOTALLY UNWORKABLE structure, that years later, up to today, is still an unworkable mess, because they forgot to ask Australians what they wanted with regard to Life Insurance advice and ignored vastly experienced Advisers who intimately understood the issues and clearly articulated the solutions.

It has ALWAYS been staring everybody in the face and was ignored due to vested interest groups who pushed their own agenda with NIL regard for what was best for all Australians, which was, as a first step, to separate risk advice from Investment advice and have a career pathway that focused on risk advice, with Education "specific" to the work being done.

Instead, as usual, we ended up with a hodge podge of rules and regulations that are not fit for purpose, that has caused untold damage to Australia and Australians, with the perpetrators still getting paid for doing the worst possible job.

Comments are closed.