The AFA has called for a return of hybrid risk commissions to their pre-LIF level of 80/20.

This is one of ten key recommendations made by the association in its submission to the Treasury’s Quality of Advice Review, which has been publicly released today.

Accompanying its first public call for a return to 80/20 hybrid commission is a tandem call by the AFA to scale back elements of the LIF commission clawback provision, which has been an equally contentious issue for many financial advisers.

Data supporting the call to return to 80/20

Of critical importance in considering the return of hybrid commissions to 80/20 is the requirement of the Treasury for submissions to provide fact-based data to underpin responses. QoA Review Question 53 asks:

Has the capping of life insurance commissions led to a reduction in the level of insurance coverage or contributed to underinsurance? If so, please provide data to support this claim.

Rather than simply offering anecdotal evidence, the AFA’s submission includes what it refers to as ‘compelling data’ which supports the fact that capping risk commissions has indeed led to a reduction in the level of insurance coverage and contributed to underinsurance. This compelling data considers two critical factors:

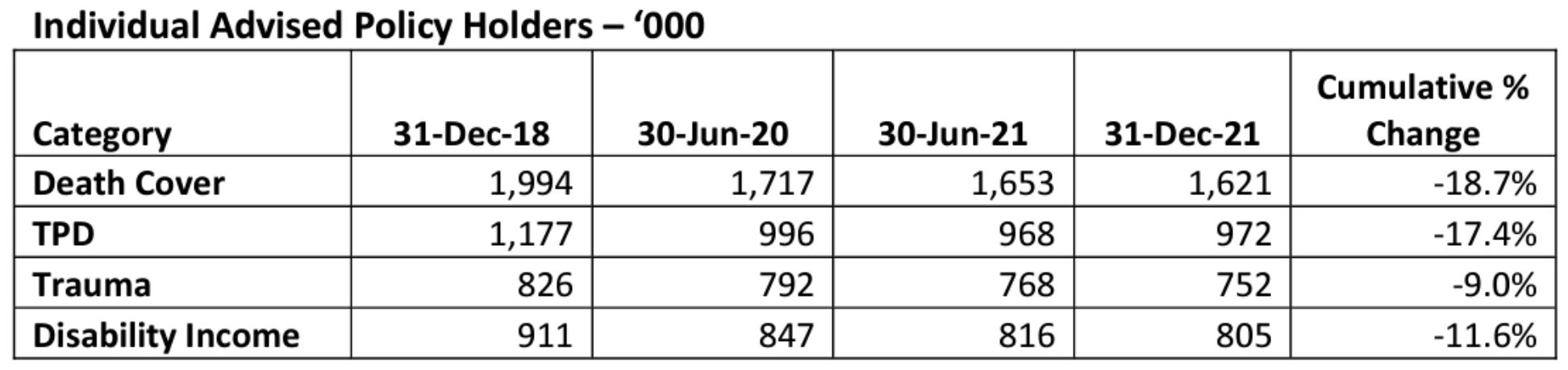

1. The decline in Individually-advised life insurance policy holder numbers

The association utilises data released by APRA to supporting its contention that the capping of life insurance commissions has had a significant impact on the number of individually-advised clients. The following table sets out this decline in advised client numbers, and is taken by the association from APRA Claims and Disputes statistics:

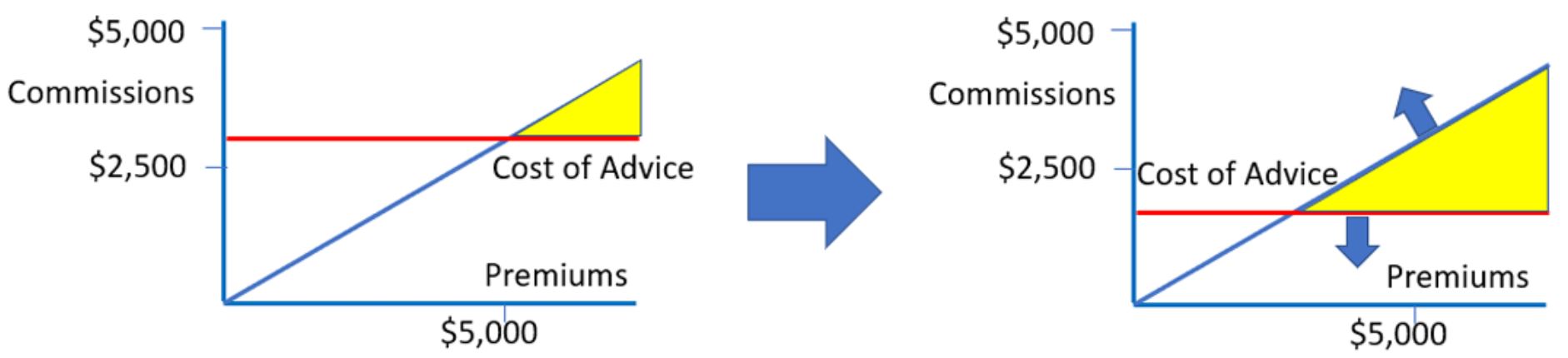

2. The cost to provide life insurance advice requires much higher premiums for this to be economically viable

In the diagram below, the association says it has assumed that the average cost to provide life insurance advice is $3,000, illustrating that – at a 60% upfront commission level – the amount of overall life insurance premiums needs to be $5,000 for the adviser to cover their costs: “This means that in recent years they have ceased providing advice to clients who are likely to have lower premiums, as it is simply not economically viable,” says the submission.

…this problem can only be fixed by a combination of increasing the commission rate and reducing the cost to provide life insurance advice

The submission advocates that this problem can only be fixed by a combination of increasing the commission rate and reducing the cost to provide life insurance advice: “In the absence of this, life insurance advice will only be available to a small proportion of the population,” notes the submission, which adds the diagram demonstrates that an increase in the commission rate and a reduction in the cost of providing life insurance advice will make advice available to many more Australians, as shown by the yellow shaded area:

In stating that there has been a very material reduction in the number of Australians covered by retail advised life insurance policies since the LIF reforms commenced in 2018, the association warns it expects that this trend will both continue and rapidly accelerate if upfront commissions were reduced further below the current 60% cap:

…LIF is contributing to an increase in the level of underinsurance, and this is only going to get worse

“Thus we firmly believe that LIF is contributing to an increase in the level of underinsurance, and this is only going to get worse, even if the current caps are kept in place,” warns the association, which also rationalises its position around the fact that its recommended hybrid model is one that existed and operated successfully in the ‘pre-LIF’ era, and which also generated a good compliance outcome in ASIC’s contentious Report 413 in 2014.

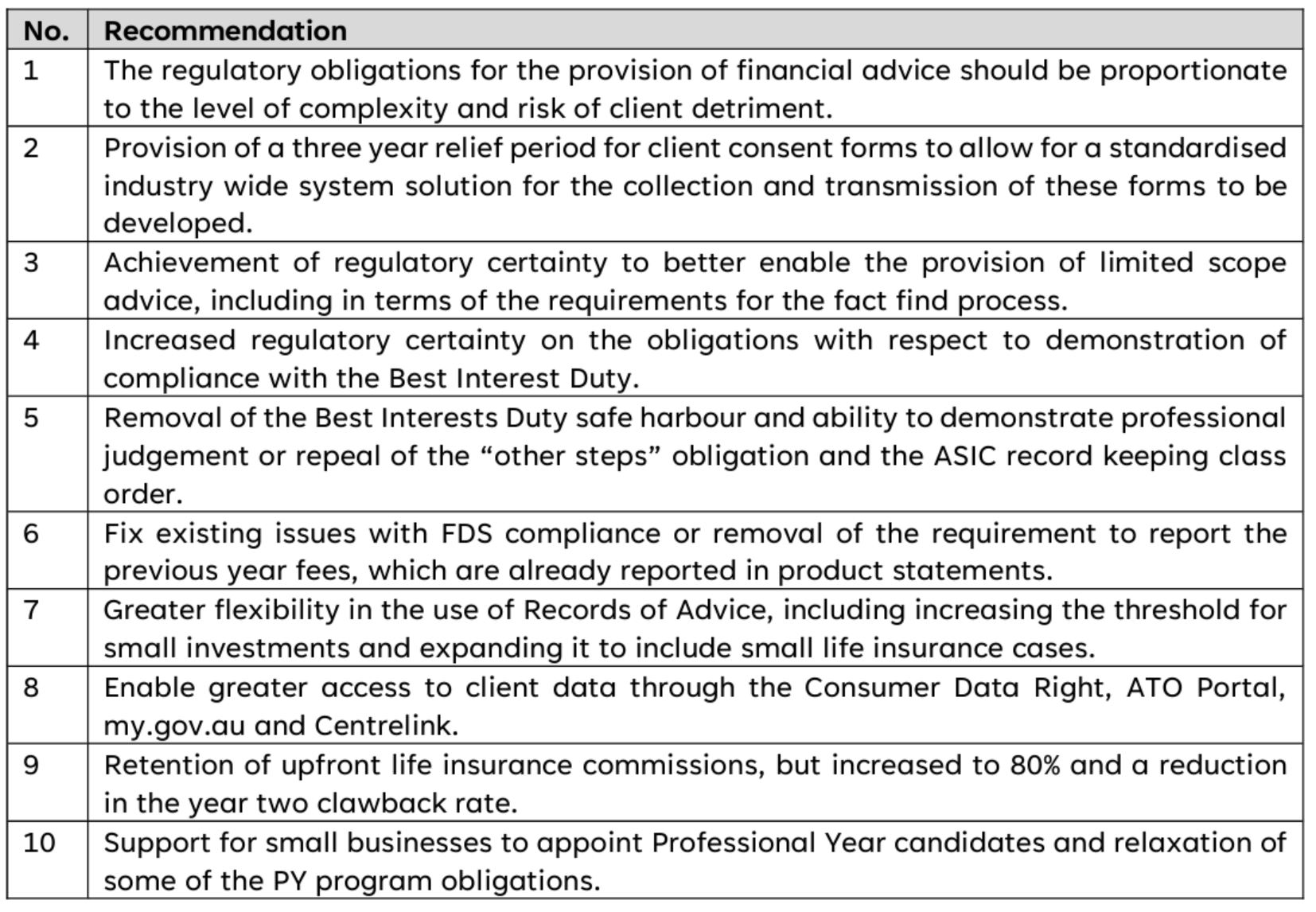

The AFA’s QoA Review submission is extensive and includes detailed reflections and recommendations on a host of other critically-important issues confronting advisers, consumers and the broader sector. Riskinfo will report other crucial elements contained in the associations’ submission, which addresses 83 questions put by the QoA Review, but where the AFA’s ten main recommendations are detailed below:

Click here to access the AFA’s Quality of Advice Review Issues Paper submission, where advisers interested in the AFA’s position on risk commissions can refer to section 7 in its introductory letter commencing on page 8, as well as page 21, and responses to questions 48 – 53.

Click here to access the AFA’s Quality of Advice Review Issues Paper submission, where advisers interested in the AFA’s position on risk commissions can refer to section 7 in its introductory letter commencing on page 8, as well as page 21, and responses to questions 48 – 53.

100/20 for commissions and 1 year clawback IF they are anywhere NEAR interested in restarting our industry! Cannot believe AFA is going ‘cap in hand’ style and pleading for 80/20 and a “reduction” in clawback period. Pathetic. 100/20 is a true reflection of the value advisers bring to clients through the assessment, application and claim periods of a policy life cycle. The time for being meek and mild is OVER – look what it got the industry – NOTHING! 100/20 and max 1 year clawback or NOTHING! This is a continuing insult to clients and advisers. The industry is stuffed, on its knees and dying and the AFA wants to pussy-foot around begging for scraps to save it!!

And….its not just advisers that are suffering. EVERY conversation I have lately with my insurance company BDM’s reveals they’re also suffering mentally and physically. They’re struggling to keep up with the increase in their workload as a result of the cost saving measures their companies are having to implement because revenue is down so much.

This industry WAS thriving and growing every year UNTIL LIF and The Hayne Royal Commission findings were released – which were all misleading and deceitful at the time and now confirmed as such. Its the law changes from them that have crucified this industry.

Like every b****y Government change these days – they’re based on the smallest minority of situations instead of them focusing on the much bigger picture – which was what WE WERE DOING RIGHT!

This industry contributed over $12 Billion in claim payments a few years back through the work of advisers. Just a few years later – through the total incompetence of a few clueless politicians, 40% of the industry’s advisers have now left and the industry is on it knees.

If any company CEO running a business did this much damage to its business like this, that CEO would have been sacked years ago – yet the stooges who screwed this industry have never been held to account for their HUGE FAILURES.

The AFA coming out now with all these recommendations now is 4-5 years too late and exactly why I cancelled my membership with them after 15 years.

Here here!! well said JADN! Man, would I love to hear from a few of the life company CEOs about why they didn’t resist the coms coming down and clawback going up! Also love to hear what they say when asked what plans do they have to support getting the coms back to 100/20 and clawback to a ‘workable’ 1 year. Are they AT ALL interested in saving THEIR/our industry? Where the hell are the life company CEOs on all of this? Crickets! They should be abjectly ashamed.

You could blame LIF, sure. That’s an easy explanation.

Or you could look at the demographic and socioeconomic shift that is happening to the country.

The 55 year olds (the target market) of 2017-18 are now 60 – the age when the needs vs cost of insurance trade off begins become unviable.

Baby boomers are all but retired and Gen-X are starting to retire. These generations are the primary beneficiaries of the property boom (the source of most of the Australia’s wealth) and the generational wealth gap is huge … which is a bit of an understatement. The median age of Australia is nearly 38 which means half the population is older than that, so Australians are fairly old.

What do you think is going to happen to the industry once that concentration of wealth has retired?

It’s not going to end well and no amount of commission is going to fix that.

Comments are closed.