There was strong reader interest this week in our report on the contention that the level of benefit written under TPD policies is impacting the long-term sustainability of the product…

The level of insured benefit written under TPD cover is emerging as an important issue impacting the sustainability of TPD insurance in Australia, according to Gen Re Regional Chief Underwriter, Bindu George.

Writing in a company news post, George states that as work environments change, medical advancements continue and economic conditions shift, the sector should carefully analyse whether TPD benefit amounts serve their intended purpose at the time of claim.

“A primary concern in TPD insurance today is the provision of benefits that exceed the necessary replacement of estimated future income loss,” writes George. “In 2022, the industry recorded its first loss for individual lump sum payments in many years.”

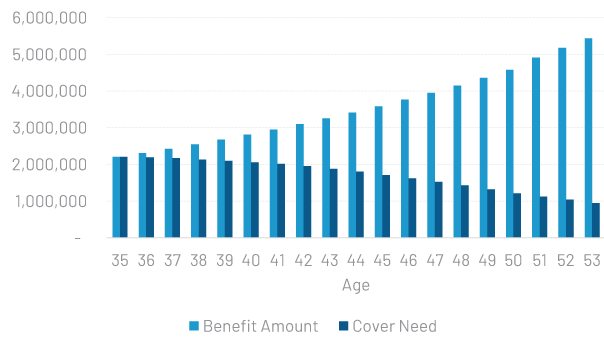

She points to “excessive benefits” playing a major role in the sustainability issues facing TPD insurance and provides this chart intended to demonstrate the excess levels of insured benefit which exist, compared with cover required over time.

“This requires a comprehensive re‑evaluation of the current benefit structures to secure the long-term viability of TPD insurance…,” says George.

She suggests a number of actions to future-proof this type of cover, including:

- Adjust income multiples to reflect realistic income progression and economic conditions

- Incorporate a more realistic model to respond to the changing need for cover over the policy term, for example by introducing negative indexation at later stages

Regional Chief Underwriter for Gen Re, Bindu George. - Implement stricter guidelines to manage the overlap between TPD and other disability benefit

- Consider setting a cap on the TPD coverage to prevent excessive claims that could lead to financial gain instead of compensating for the actual loss

- Balance indexation to keep pace with inflation without causing excessive increases in cover amounts

- Regularly review and adjust indexation rates to ensure they remain appropriate and sustainable

- Ensure consistent treatment of tax impacts at both the benefit calculation and the claim stages

- Use post-tax (net) income for benefit calculations to accurately reflect the policyholder’s financial needs and ensure benefit amounts align with the income required to replace estimated future income loss

George states: “By committing to long-term sustainability, insurers can ensure that everyone is protected against life’s uncertainties.

“The sustainability of TPD products relies on striking a delicate balance between affordability for consumers and the financial viability of insurance providers.”

She states that innovation in TPD insurance products is crucial for maintaining this sustainability.

“By revising benefit structures and implementing robust financial underwriting practices, the sector can enhance the long-term sustainability of TPD insurance,” she says

Riskinfo readers can click here to read the full article.

So a reinsurer is arguing that TPD benefits are being calculated too high by advisers.

There is a reason that strategy has been developed and it is to be sourced in the AFCA action of the IP nuclear option on 1 October 2021: the significant step to reduce the value of an age 65 benefit period in IP, cut off by there being ONLY a two-year own occupation guarantee.Today's age 65 benefit period can in no way be compared to what was available prior to 2021.

One assumes that APRA, who never consulted advisers, did in fact consult the 5 or so reinsurer's about the implications of that drastic action. Most insurers say they were never consulted by Apra, at least not in a meaningful manner. Did the reinsurer's have a facility to register their concerns.?

There are a number of FASEA standards which could severely impact on an adviser who doesn't take the long-term view as to the value, or non-value, of recommending a post 2021 age 65 benefit period.

Could it be that significant increase in advised TPD lump sum insureds that have occurred since October 2021 could have been reasonably predicted if only Apra had read the FASEA Code ( and consulted advisers) and realised that advisers had very little choice other than to recommend increased sums of own occupation TPD cover as an income supplement to compensate for the possible loss of income in long-term disability or the recommendation of a five year benefit period to avoid the rubbish that is NOW contained in a policy with an age 65 benefit period.

Comments are closed.