New research which highlighted a potentially significant advice opportunity – for all advisers – attracted strong reader interest this week…

Australians approaching retirement are financially engaged but many remain unprepared for the transition from accumulating superannuation to drawing a retirement income, according to new research from TAL that highlights a significant advice opportunity.

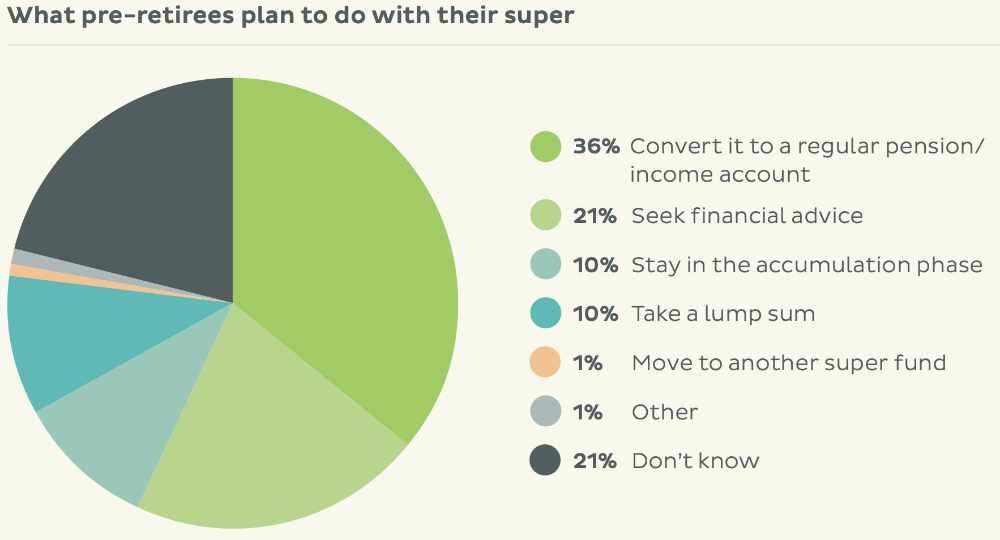

The insurer’s second What I Wish I Knew About Retirement study reveals one-third of pre-retirees have taken no action to prepare for retirement and one in five do not know what they will do with their super, despite two-thirds describing themselves as engaged or highly engaged with their finances.

The research also points to growing demand for income certainty, with lifetime income and inflation-linked income ranked among the most valued retirement product features.

Shaun Bransdon, TAL’s GM Retirement and Wealth, said: “People care deeply about their financial futures and they’re paying attention, but we don’t see that in the actions they’re taking to plan for this critical life stage. Many feel they don’t have all the information they need.”

He said 64% of pre-retirees trust their fund to advise on retirement needs.

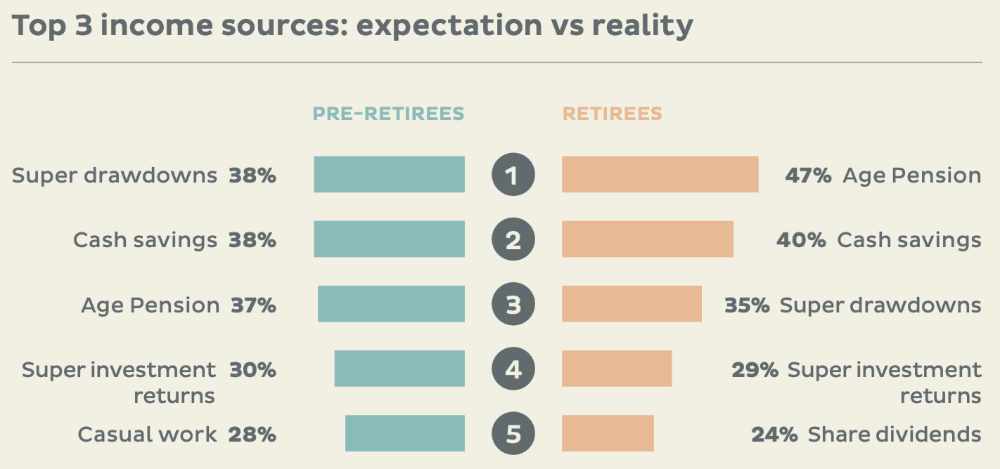

This year’s research shows almost half expect to have less spending power in retirement, while the proportion of pre-retirees planning to work past age 70 has jumped from 27% in 2024 to 36%.

While 33% of pre-retirees expect their retirement to last longer than 20 years, almost half expect their super to run out before then.

Meanwhile, nearly half of retirees surveyed (48%) had taken no meaningful action to prepare for retirement, up from 39% in 2024.

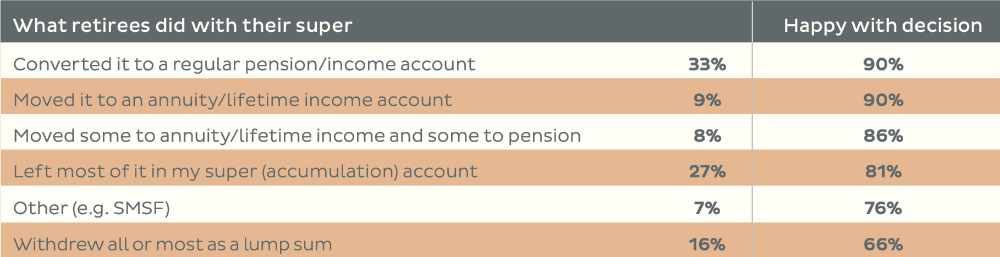

The research revealed significant differences in satisfaction based on what people did with their super when they retired.

Around 90% of retirees who chose pension accounts or lifetime income products were satisfied with their decision. This compared with 81% who left their super in accumulation and 66% who withdrew lump sums.

In what appears to be a significant and untapped opportunity for all advisers, the report notes just 38% of pre-retirees are familiar with how these products work and 87% would want to find out more if their fund offered a lifetime income product.

“Without certainty about future income, even retirees with adequate savings may default to conservative spending. Product design can help, giving people confidence to enjoy their retirement while knowing their essential needs are covered,” Bransdon said.

Graphics and data / TAL’s What I Wish I Knew About Retirement report.

Click here for the full report.