The Government is seeking industry consultation on the prospect of mandating universal insurance definitions, terms and exclusions within MySuper products.

This move comes in the wake of the Banking Royal Commission recommendation 4.13, in which the Commission advocates that:

Treasury, in consultation with industry, should determine the practicability, and likely pricing effects, of legislating universal key definitions, terms and exclusions for default MySuper group life policies.

The rationale for this recommendation is based on Commissioner Hayne’s finding that insurance contracts “…can often be difficult for the average consumer to navigate and understand.”

In his final report, the Commissioner added that subtle differences in definitions, terms and exclusions from one policy to another can make the task of comparing policies particularly challenging. He noted this can affect:

- When an individual can claim under a policy

- The cost of insurance premiums

- How much superannuation an individual will have at retirement

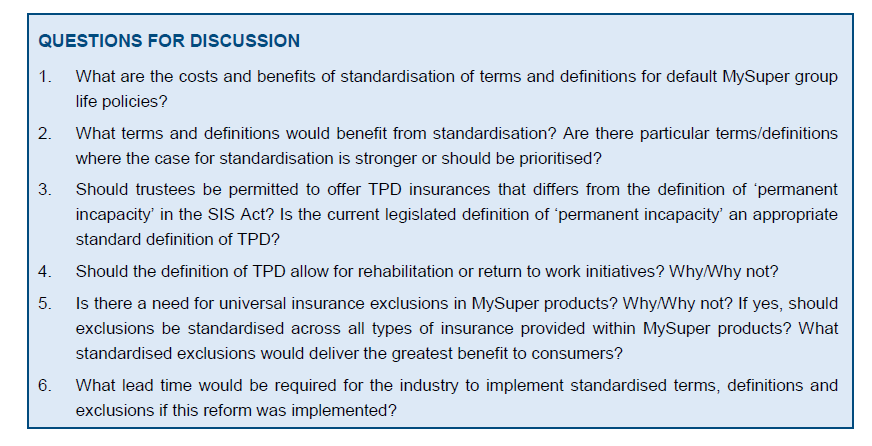

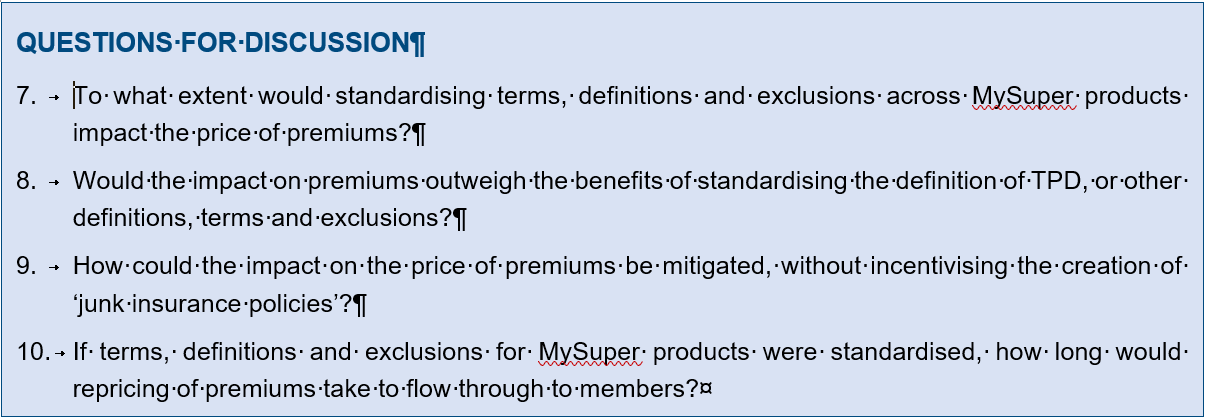

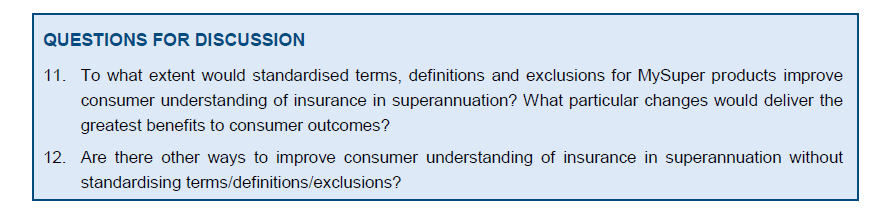

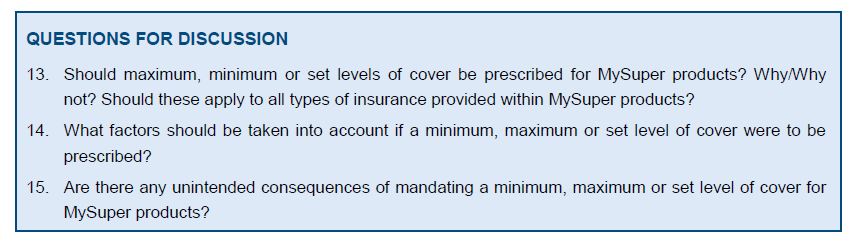

With these issues in mind, the Government’s consultation paper is seeking industry feedback around fifteen questions under five different sections:

- Standardising TPD and other terms, definitions and exclusions:

- Impact on premiums:

- Improving consumers’ understanding of insurance in superannuation

- Merits of prescribing minimum, maximum or set levels of cover

In its release, the Government notes its focus is on placing the interests of superannuation members first, ahead of the interests of the superannuation funds themselves.

In its release, the Government notes its focus is on placing the interests of superannuation members first, ahead of the interests of the superannuation funds themselves.

Click here to access the Government’s consultation paper for Universal Terms for Insurance Within MySuper, where the Treasury is requesting email submissions to be sent by 26th April to:

superannuation@treasury.gov.au

What a mess. Sounds easy. Its not! So do ALL the funds all adopt the nasty Oz Super “rehabilitation test” in TPD & watch premiums for those funds currently without a Rehabilitation test GO UP. What about transparency – let the funds disclose the commissions paid to the Trustees for new members, and bonuses for delaying claims in a KPI assessment quarter, Default insurance requires personal advice – particularly that cover decreases after age 37. Rumour has it some interesting class actions are afoot.

Comments are closed.