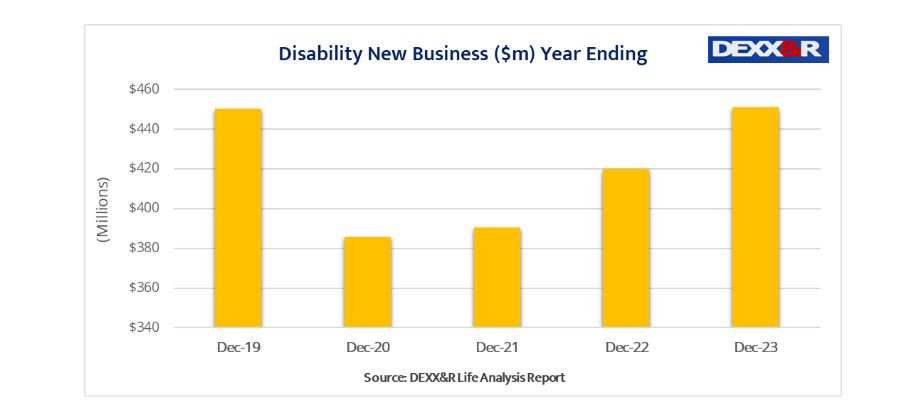

Disability income new business increased by 7.3% in the year to December 2023, says DEXX&R’s latest Life Analysis Report.

The research firm says disability income new business rose to $451 million over the year to December 2023, up from the $420 million recorded in the 12 months to December 2022.

The disability income new business includes CPI and age-related increases along with policyholders voluntarily increasing their coverage; DEXX&R’s MD Mark Kachor telling Riskinfo about 60% is actual new business.

He says the 7.3% increase could be seen as the ‘gross’ new business figure and that it does offer consistency over time and is “what pays the bills”.

Kachor noted too that net new business varies over time, pointing to the large books held by insurers which do not take on any new business and where the only new business is that which is age or CPI-related.

In the same period, lump sum new business premium was down 5.4% to $910 million from the $962 million recorded in the year to December 2022, which follows a small slip in the year to September 2023 (see: IP Sales Rebound).

Quarterly Data

In the December 2023 quarter, disability income new business at $113 million was down 12.3% from the $129 million recorded in the September 2023 quarter, but 2.4% higher than the $111 million recorded in the December 2022 quarter.

DEXX&R notes that during the December quarter individual lump sum new premium decreased by 9.7% to $214 million, $23 million less than the $237 million recorded in September 2023 quarter.

The December quarter sales of $214 million were 12.6% lower than the $245 million recorded in the December 2022 quarter.

Discontinuances

Discontinuances

The report also notes that the Attrition Rate for disability income business increased to 10.9% in December 2023, up from 9.8% at December 2022.

DEXX&R says discontinuances continue to climb from the 9% low recorded in December 2020 immediately prior to the release of a new range of disability income products following the APRA intervention and release of conforming products in 2021.

The firm says that individual lump sum discontinuances saw the Attrition Rate increase to 10.1% in December 2023, up from 9.3% at December 2022.

The Attrition Rate calculates discontinuances as a percentage of in-force premiums.

7% is substantially less than the average money-weighted annual price increase (older people pay much more and have much higher percentage increases). Even with 10% delinquency that is only 17% and therefore perhaps a small increase due to new business – 2-4%?

Comments are closed.