While decisions grounded in ethics are part and parcel of an adviser’s professional life, a specialist in ethical leadership says there is not always only one right answer when it comes to making a decision.

In delivering a presentation where he posed a series of ethical dilemmas, Life Risk Strategy coach Mark Neil gave attendees at Riskinfocus 25 Risk Advice CPD events four scenarios to challenge their decision-making.

Neil, who has spent almost 40 years in the industry, including in risk roles, is recognised as one of the pre-eminent insurance strategy specialists in the insurance market.

During his PPS Mutual-sponsored presentation, he set out to illustrate decisions that balanced fair client outcomes with professional responsibilities, with audience members voting via their phones.

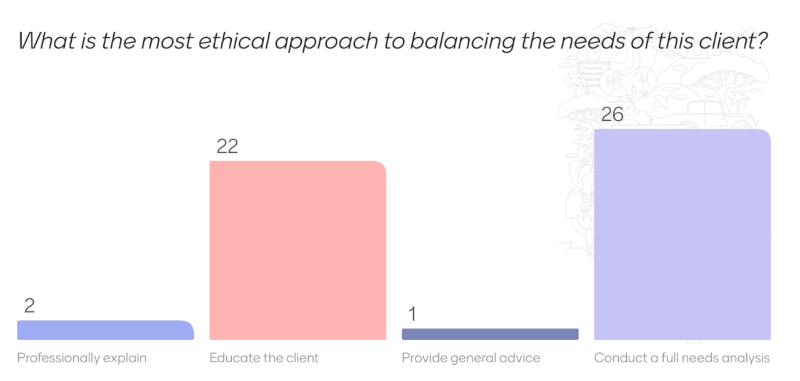

Dilemma 1: Ethics in advice recommendations. What is the most ethical approach to balancing the needs of this client?

In a common scenario, where a client seeks to limit their cover, Neil said advisers face a dilemma and gave them four possible answers.

- Professionally explain that you are unable to provide transactional advice

- Educate the client by providing clear and straightforward information to help them understand the various risks, insurance options, and their benefits. Recommend best IP

- Provide general advice only or refer to another adviser

- Conduct a full needs analysis and recommend the best strategies and policies. If implementing only an Income Protection policy, document the client’s decision-making process to demonstrate good faith. Follow up and review

The majority of voters favoured option two, educating clients about risks while conducting a full needs analysis to recommend a tailored solution.

Neil stressed advisers should avoid transactional approaches, instead fostering informed decision-making to ensure clients understand the implications of their choices.

He also suggested clients repeat back to the adviser what they are agreeing to – to confirm they comprehend the advice given.

For clients who refuse good advice, Neil said there is nothing unethical about refusing to help a client.

“You can always refer them somewhere else,” he said.

Dilemma 2: Advocacy when a claim is denied. Considering the potential impact on all stakeholders, what course of action would best uphold ethical principles?

This second dilemma focused on a client whose TPD claim was denied due to complex medical criteria and a less than helpful medical specialist.

- Remain neutral and provide the client with information regarding the complaint process

- Advocate for and support the client in challenging the claim denial. This involves researching the case, especially the medical evidence, helping draft the complaint, and potentially advocating against the insurer

- Refer the client to a claims advocate service for review and to formulate a plan of action to achieve a favourable claim resolution

- Provide information on the Australian Financial Complaints Authority (AFCA)

Neil cautioned against clients pursuing costly legal action, which could consume 30% to 40% of any payout.

Instead, he favoured advisers supporting clients by advocating with insurers and doctors, or referring them to specialised claim support services.

The majority of audience responses agreed with this approach to navigate the high bar of “permanent” disability definitions.

Dilemma 3: An adviser hears a client being paid under an income protection plan is working. Given the conflicting interests at play, what decision aligns most closely with ethical guidelines?

- Remain silent and do not report the discrepancy. This choice preserves the relationship with the client but compromises ethical standards

- Contact the client, inquire about their work status. If applicable, offer them a chance to come forward to the insurer to lessen the impact. Emphasise the importance of not falsifying documents

- Explain how fraudulent claims can increase premiums for all policyholders. Offer to mediate with the insurer before any formal action is taken

- After a final discussion, express your concerns. If the client does not rectify the situation, terminate the relationship. Document the process, notify in writing, and report the suspected fraud

Most of those who voted selected option two, with option four also garnering support.

“This is a case I had a few years ago,” said Neil. “I worked with an adviser through this very issue.

“The adviser had known the client for 15 years and didn’t know what to do.

“The client said they’d been paying the policy premiums for 15 years and wanted to claim another couple of months.

“The adviser told the client he could help them any more and reported it as a possible fraudulent claim.”

Dilemma 4: What is the most ethical form of risk advice revenue?

- Transparent commission-based only

- Hybrid model a combination of fees and commissions with clear disclosure of fee structure e.g. initial, ongoing and claims processing

- Fee only compensated solely by the fees paid by the clients and all product commission removed. This can include hourly fees or flat fees for service e.g. initial, ongoing and claims processing

- Fee only with a rebate for any commission received. This can include hourly fees or flat fees for service e.g. initial, ongoing and claims processing

Most voters opted for option two, the hybrid model, with option one coming in second.

Neil addressed the shift from commission-driven to hybrid fee-and-commission models, reflecting a move toward transparency and professionalism.

He noted that 63% of advisers now adopt a hybrid model, charging initial advice fees alongside commissions to cover implementation risks, such as underwriting rejections.

Ethics are nothing more than improving trust and transparency…

This cross-subsidised approach, he explained, helps ensure advisers are compensated for complex cases, even if policies aren’t implemented.

He reassured advisers that ethical compensation aligns with fair client treatment, provided services are clearly explained.

Neil also challenged the notion that all clients should receive identical service, stating that client segmentation can be based on revenue contribution.

He argued that ethical treatment doesn’t mean uniform service, but rather proportional value, comparing it to tiered service packages.

“Ethics are nothing more than improving trust and transparency as we move from a sales culture to a profession,” he said.

A for a few decades ago I had an experience when IP claimant was actually seen driving to the scene of his work while on claim. I did not become aware of this situation until the insurer moved to stop the claim. The claimant thought he was being a bit too smart but the claim was stopped after that little episode and subsequently his condition actually worsened, but the insurer refused to pay ball.

Since that time, I have a standard presentation to each and every of my clients for whom I going to represent in a claim situation: "I will represent you to the best of my ability, and fight tooth and nail on your behalf for as long as it takes, and not charge a fee. BUT, if you lie to me, or provide me with any information that is not accurate to my endeavours to represent your situation, then I will cut you loose"

Funnily enough most people readily agree. But you have to eyeball the client and then note the conversation, preferably recording it on a digital device. And then if you do cut the client loose, confirm it in writing, but be aware of libelling the client. And yes it would be prudent to refer that particular client to a specialist claims handling company or perhaps even a "no-win, no-fee" solicitor.

Comments are closed.