Advisers have been urged to adopt a more structured and proactive approach to income protection advice for small business clients.

Speaking at last week’s 2025 FAAA Congress in Perth, Acenda’s Partner Education Manager Marshall Ross urged advisers to adopt a more structured and proactive approach to income protection advice for small business clients.

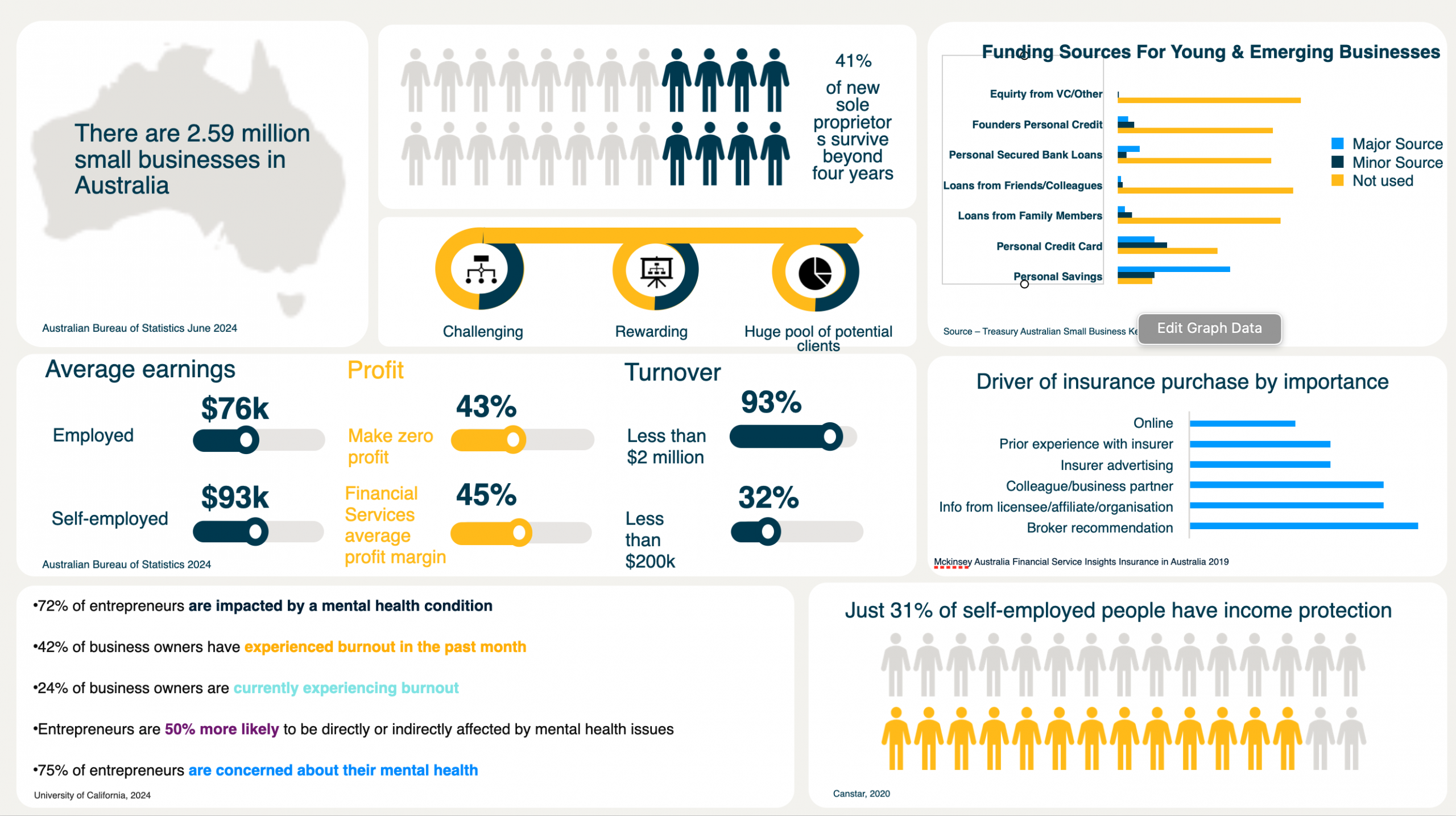

He warned that this cohort – there are 2.59 million small business owners nationally – remains both “highly exposed” and “chronically under-insured,” despite many being aware of the financial risks of running a business.

Addressing advisers at the three-day event in Perth, Ross said too many business owners operate under a “false sense of security” regarding income certainty and business continuity.

Despite the perception that entrepreneurs rely on sophisticated funding structures, “the data shows something very different,” he said.

“Most people start their business on personal savings and personal credit cards. That starting point shapes their behaviour for years, and often shapes their blind spots.”

Ross said advisers should frame conversations around problems business owners already recognise, particularly the tension between their two competing roles: business owner and household decision-maker.

“There’s a natural conflict between protecting the business and protecting the family,” he said. “And that’s exactly where high-quality advice adds value, by creating buffers that reduce exposure rather than amplify it.”

He encouraged advisers to begin risk discussions with income, describing it as the “foundation stone” for nearly all financial goals, personal and business alike. He suggested owners of small businesses routinely underestimate income volatility and overestimate the business’s capacity to keep paying them during illness or injury.

“Variance equals risk,” he said. “Small businesses have more variance, fewer buffers, and less certainty than salaried workers. Our job is to help these clients understand what that means in real terms.”

Ross also recommended linking income to future business value, noting that clients engage more deeply when they understand they are building something that needs protecting.

A significant part of his presentation focused on the practical steps advisers should take when determining appropriate income protection benefits for self-employed clients.

He outlined a five-step process for identifying personal exertion income, which includes understanding business structures, reviewing drawings and distributions, and applying consistent add-backs such as non-cash items, one-off costs, and discretionary expenses.

His five steps are:

- Establish: Review the business information, nature of operations, structure, and ownership interest

- Net income: Personal exertion income minus business expenses

- Identify: Associated payments such as management, consulting, or service fees

- Ignore: Drawings, distributions, and dividends—trace these back to their source

- Add-backs: Apply add-backs (non-necessary business expenses) to net income

- Ross also urged advisers to reframe insurance in terms business owners already understand – liquidity.

“Liquidity keeps a business alive,” he said. “It buys time, freedom, and better decision-making when something goes wrong.”

He also cautioned advisers not to overlook business expenses cover, arguing that income protection alone is rarely sufficient.

“You can’t expect the client’s personal benefit to carry both household expenses and business overheads. That’s when clients start cannibalising their own income.”

Ross said advisers should address objections with clarity rather than confrontation and concluded that the real value of advice is not the product or the premium, but “confidence, clarity and certainty”.

“People pay for how advice makes them feel,” he said. “Income protection isn’t just a product; it’s a buffer that protects the future they’re working so hard to create.”

Key points

- Unique: Business owners’ needs are distinct and require professional advice

- Education: Helping clients understand their situation is essential

- Expectations: Client expectations are within your control – your advice must align with them

- Value: Advice is valuable because it is personalised and solves problems, not because of its price

- Appropriate: Demonstrating the “why” means linking recommendations to the client’s specific situation