Net adviser outflows took a breather in the third quarter of 2020 with a net decline of just 1.8 percent from the previous quarter, according to Adviser Ratings Adviser Musical Chairs Report.

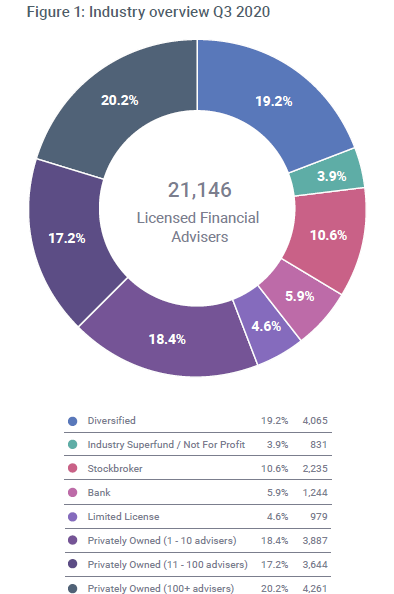

It found that by the end of the third quarter the adviser population had reduced to 21,146, representing a net decline of 388 advisers (1.8 percent) from Q2 2020 which it says is “comfortably the lowest quarterly decline since the industry started net contraction in 2018”.

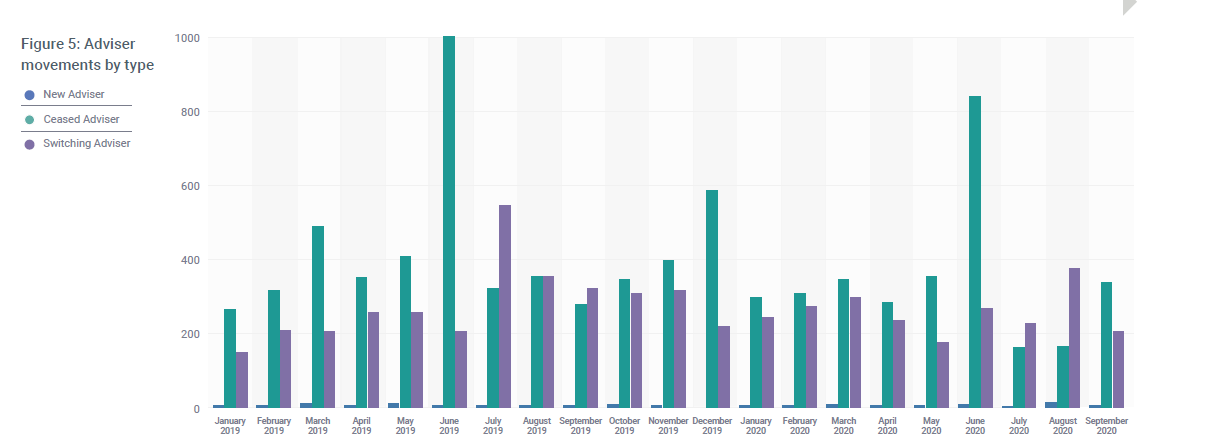

While 660 advisers (3.1 percent for the quarter, 12.4 percent annualised) left the industry in Q3 2020, the overall reduction in adviser numbers was 388, as:

- 14 new advisers joined the industry

- a further 258 transitioned back after being previously ceased

The report also found that 778 advisers (3.6 percent and 14.4 percent annualised) changed licensees in the quarter, slightly above trend of the past 18 months which was at 12 percent annualised.

It says that total adviser movement was well down from prior quarters, with switches exceeding exits only once before in Q3 2019 in the 18 months that it has been producing the report.

“Is it possible that advisers, notwithstanding their fair share of bruises from regulatory and market headwinds, are taking a more positive long-term view on their future in the industry?”

The report says that, for example, with ASIC extending exam completion by 12 months to December 2021, many advisers may have taken advantage by avoiding the exam altogether to eke out another year in the industry before leaving.

However, it notes that another 1,500 advisers completed the exam in August and a further 1,900 registered for October and November exam sittings.

“If all those advisers were to pass the exam, this would push the completion rate to approx. 55 percent of registered advisers nationally.”

Adviser Ratings also highlights that in the last quarter there has been “a substantial increase in the narrative, coming from all corners of the industry, to reduce compliance red-tape to lower the cost of advice and simplify requirements for providing limited advice”.

Nevertheless, it says there is unlikely to be material change for the immediate future until some of the “blockers” to advice simplification that are routinely mentioned are addressed. This includes current requirements under best interest duty and the FASEA code.

“ Further, in terms of additional changes in the pipeline that may complicate matters, the Government has indicated that the single disciplinary body to oversee FASEA compliance and the compensation scheme of last resort would not be on the table until the middle of 2021, and it is not clear yet how, nor when, the other recommendations from the Royal Commission will be implemented,” the report states.

Click here to view the full report.

14 new advisers joined the industry

I think that’s the key takeaway.

The rate of advisers leaving the industry might have slowed but in my view this is because they have nowhere to go. With the sale of their businesses devaluing so much many advisers likely feel they’re better off staying put. ‘The devil you know’, kind of thing…

There is light at the end of the tunnel, as both ASIC and the Government have started to recognise that the LIF / FASEA regime is causing untold damage.

There has never been a better time to keep pursuing the changes that are needed, though the current pace and time frames are still insufficient to stop the exodus of advisers and even though there has been a slow down, mainly due to the extra 12 months grace, The main issues that are the cause of advisers exiting, have not been addressed and perceived remedies being thrown around, will not work.

30,000 risk advisers are needed, as there has never been a better time to provide risk advice, the only issue being, new clients carry too much risk and expense to justify taking them on.

As Leeroy mentioned, 14 new advisers joining is a clear indication that there is a gap between what the Government has continually been promoting and the real world, where there is a triple whammy of too few advisers, too many exiting and only a trickle of new advisers coming in to replace those who have left.

The minor detail of new advisers not having any experience and real world knowledge,

ie; most Australians prefer to get advice from an adviser who has more than a bit of paper to show, has also not been properly addressed.

Comments are closed.