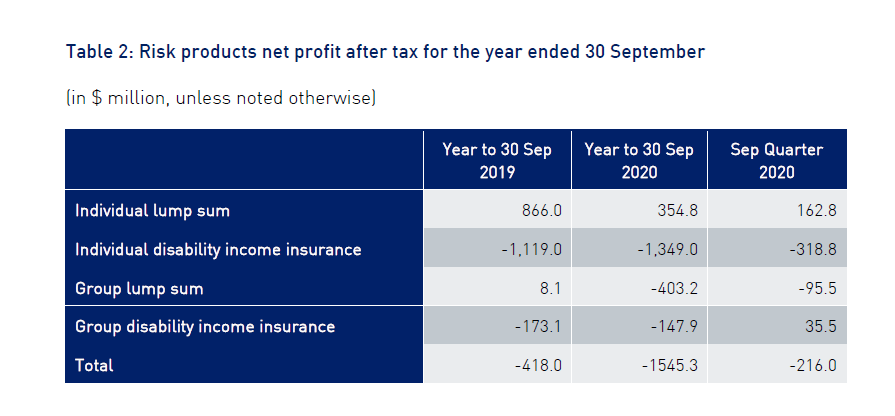

Risk products reported a combined after-tax loss of $1.5 billion for the 12 months to September 2020 although individual lump sum continued to provide a slight glimmer of silver-lining for the industry.

APRA’s Quarterly Life Insurance Performance Statistics publication for the September 2020 quarter shows this combined loss compared with a $418 million loss in the September 2019 year.

APRA says that the performance of all risk products deteriorated apart from the individual lump sum product.

The report shows it made a a $354.8 million profit for the year to September 2020, however this compared with a $866 million profit for the September 2019 year (also see the June quarterly report: Performance of Risk Products Deteriorates).

A statement from APRA says in particular individual disability income insurance (also known as income protection insurance) “…reported a substantial loss, primarily driven by loss recognition as adverse claims experience persists.”

DII recorded a $1,349 million loss for the September year compared with $1,119 million in the year to September 2019.

1) Why is the biggest issue in the industry the lowest headline?

2) Who will be first to raise their hand and admit income protection is a terrible idea?

Edit: Individual IP is losing money almost 4 times as fast as Individual Lump Sum is making money. If this were a stock market it would be called a crash. If it was General Insurance it would be a catastrophe. But this is Life Insurance so adviser commissions are the number one headline.

I think Leeroy there are issues here that go far further than it being a bad product.

Its not the product nor the philosophy behind it ! It is the constant “tinkering” with it and the need for Insurance Companies to ad and add and add more and more benefits that they think is attracting the client to their product and of course the initial actuaries ideas { not tried and proven } that have caused these massive claim issues. Clients have become more “savvy” in their thinking and now look very closely to see if they can! claim rather than should they ? An example was AC&L’s original covers that gave long term benefits { Lifetime accident cover and Age 65 benefit periods to heavy blue collar workers! by the time the realized the issues they created it was too late { Guaranteed renewable cover sorted that out ? }

Now they are all rushing to increase premiums dramatically and reduce or eliminate additional benefits that have caused major claims increase’s eg { day 4 accident benefits } and the list goes on.

I have no doubt and have been saying it for sometime the simplicity of these products is the only way out of this mess they have created. 2-5 year benefit periods minimum waiting period or maybe varied waiting periods between accident and illness on the same policy ? removal of unnecessary “special” benefits that either never get used or are that convoluted half of today’s claims teams don’t understand them ! how or when they started and even if the client qualifies.? The product is viable and needed by Australians and our health system. Without it the problem is worse.

It will happen ! It has to so be prepared !

I think Leeroy there are issues here that go far further than it being a bad product.

It’s a bad product.

It is the constant “tinkering” with it and the need for Insurance Companies to ad and add and add more and more benefits that they think is attracting the client to their product

This occurs because advisers rely heavily on research ratings. A 95% product looks better than a 92% product on a SOA but no one ever really questions why.

The product is viable

I don’t think we read the same article?

Comments are closed.