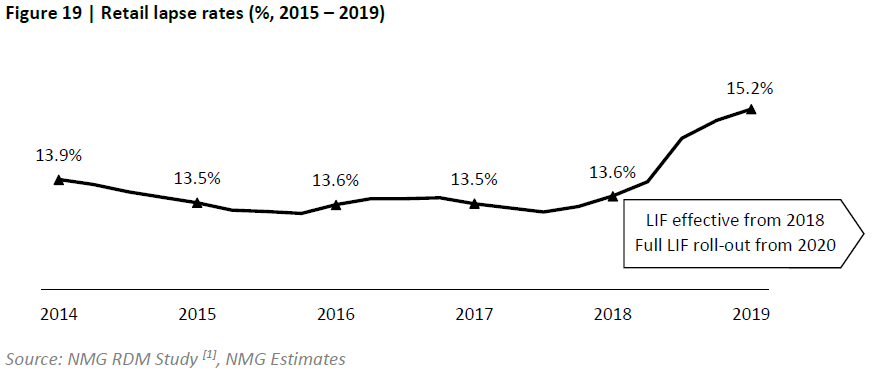

Retail lapse rates have surged since the implementation of the Life Insurance Framework reforms, but the causes are not related to churning.

This is one of many findings documented by specialist financial services consulting firm, NMG Consulting, in its Australian Life Insurance Market Research Report, which was released in 2020.

The following chart, taken from the report, paints the picture:

In its report, NMG notes it is an historical assumption that higher lapse rates are primarily a function of churning. But its research findings appear to contradict this assumption.

In what may be considered by some industry stakeholders as ironic, the consulting firm attributes this sharp increase in retail lapse rates in recent years, represented in the above chart, not to churning, but to these three primary drivers:

- An increase in ‘partial lapsation’ (reductions in cover and premium)

- An increase in compulsory lapses (policy lapsing at maximum age)

- Policy holders lapsing out of the system (cancelling the policy with no replacement)

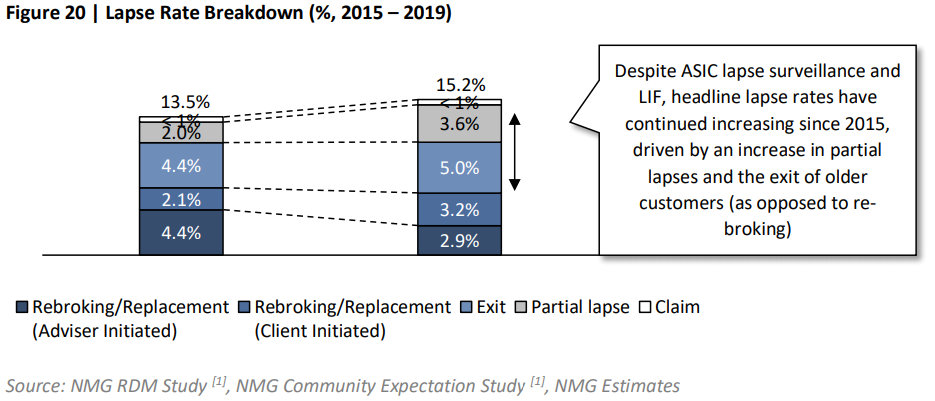

Comparing lapse rates in 2015 with 2019, the report then breaks the causes into their components:

The chart breaks down ‘rebroking’ into adviser-initiated and client-initiated components, and the report goes on to reflect that it is challenged to differentiate between what it refers to as ‘adviser benefit driven’ lapsing (churning) and ‘customer benefit driven’ lapses.

…adviser driven re-broking is unlikely to be a significant element of re-broking

While NMG says it cannot be definitive because it hasn’t had access to case-by-case file reviews, its report nonetheless draws some conclusions when it notes:

“…we can reasonably assume that in the current environment (with ongoing ASIC lapse surveillance and file reviews) and in the context of heightened scrutiny by licensees as well as insurers, adviser driven re-broking is unlikely to be a significant element of re-broking.

The overall picture painted by these research findings appears to support the contention held by many advisers and other industry stakeholders that the relative incidence and impact of churning life insurance business in the Australian market – an issue of critical importance in the shaping of the Life Insurance Framework reform legislation – appears to be somewhat anecdotal in nature, as opposed to being supported by any fact-based research or rigour.

…international markets with materially higher initial commission rates show consistently lower lapse rates

The research paper appears to reinforce this point in adding that, if anything, an inverse relationship exists between initial commission levels and lapse rates. It reflects that “…international markets with materially higher initial commission rates show consistently lower lapse rates.”

In providing context, NMG Consulting’s Australian Life Insurance Market Research Report was commissioned by Australia’s big four life insurance groups in conjunction with the AFA, FPA and FSC, which in turn informed the basis of this group’s ‘Choice & Access to Life Insurance’ (CALI) campaign in June 2020 (see: Underinsurance Will Worsen…).

The CALI campaign’s focus at the time related to various issues including community attitudes and expectations, the future outlook for advised life insurance, international comparisons, regulatory reform and affordability. While lapse issues were included, they formed a single component within a broader narrative.

So, 90% of the increase in lapse rates is due to clients cancelling. That will partially be a response to the large premium increases but it could also be because advisers have stopped proactively reviewing clients to see if there is something better. I wouldn’t be at all surprised if a lot of clients who cancelled would have continued with their insurance if they received a shiny new policy sold by a sales person to them, even if that policy was equal to the old one.

ASIC admitted long ago that churn from advisers was very low, yet they still continued with their witch hunt and continued on their path of making it no longer viable to be a risk specialist.

Clients do not want to cancel their Insurances after all the time it took them to set up their Superior Retail policies with their Advisers help.

The reason for lapses is easy to understand and has always been the same reason for the vast majority of cases.

1) large premium increases. 2) Clients changing circumstances.

This sounds absurd considering that many hundreds of millions of Tax payers dollars has been spent trying to find the holy grail of “WHY” when the answer was always in front of them, being, ask the client.

This simple solution was ignored and brushed aside, as why would you ask the people who actually pay the premiums, when you can pay “experts” to analyse data and allow them to theorise and develop strategy that includes their ongoing advice at a cost of millions of dollars, that will take years to come up with the answer to this conundrum.

Common sense and an ability to recognise and bypass Bulls–t when it is presented as T-bone steak, is very much lacking with Government and Regulators and is the reason why all Australians are in the predicament we face today.

Churn was the supposed main reason for the beginning of all the chaos we have been through over more than 7 years and has been known as a lie for most of that time.

It is time for the Government to apologise and recognise that their misguided, Utopian Regulations are the MAIN cause of lapses and for them to reverse the damage.

Totally agree Jeremy. Does anyone know if the findings in this report will be submitted to the govt?

And you can bet your family home on it that ASIC still won’t listen or take notice of this information – nor John Trowbridge who probably still believes he’s a maestro with what he came up with for LIF.

Its just laughable when you consider industry advisers screamed this was the case from the highest mountains yet no-one listened. Well guess what ASIC, Trowbridge and all you self-confessed geniuses – US ADVISERS TOLD YOU THIS!!!

Yes LIF was supposed to be the panacea but has turned out to be a poisoned chalice. As stated above we warned you but you did not listen!

If you are one of those faceless people involved in making that ideological decision then you now have blood on your hands from so many Australians that would have been insured properly but are not sadly.

Shame shame shame.

Comments are closed.