The Actuaries Institute’s Disability Insurance Taskforce released its final report this week into the plight of individual income protection insurance sector, sending a positive message to the industry that “…real momentum for change” is unfolding.

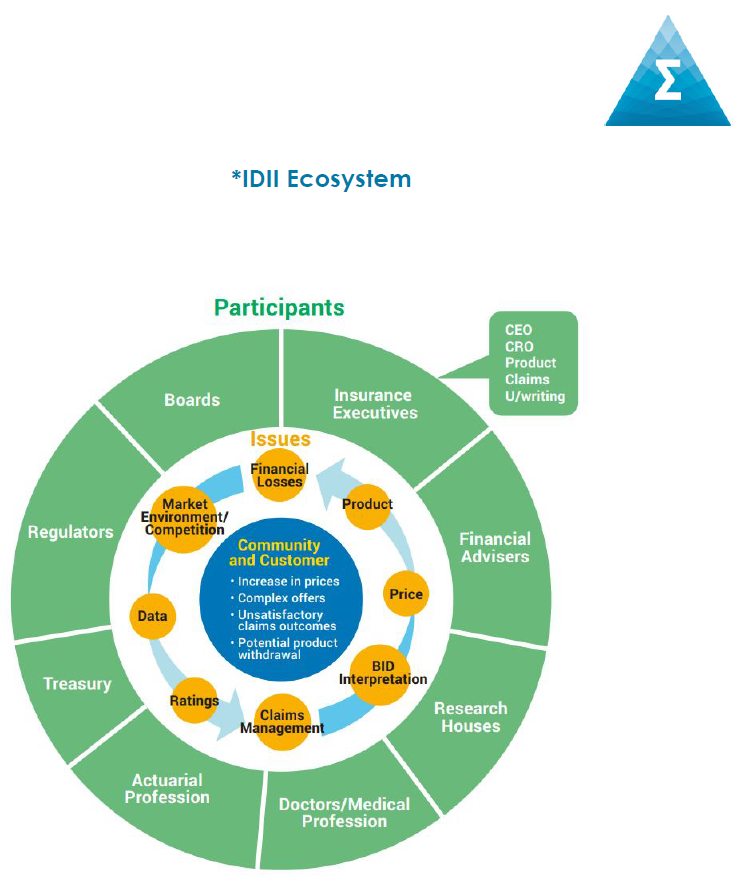

While cautioning that the individual disability income insurance (IDII) market continues to face significant financial stress, the institute’s Disability Insurance Taskforce nonetheless holds that it has developed a path forward for the industry, which will “…involve change and contribution by the many participants in the IDII ecosystem.”

Led by senior actuary and former APRA deputy chairman Ian Laughlin, the Taskforce’s recommendations are intended to reflect consultation it has undertaken and feedback received from industry stakeholders including:

- Policy makers and regulators

- Insurers

- Consumer advocates

- Ratings houses

- Industry representative bodies such as the Financial Services Council

…the Taskforce set out to have a customer-centric view

Laughlin said the Taskforce set out to have a customer-centric view and to commit to tackling issues from a professional and objective standpoint. “The Institute established the Taskforce to analytically assess the many factors at play in the retail disability insurance market and to manage a process where all parties tried to understand the issues and how to improve outcomes for customers,” he said.

The Recommendations

The main report details a large number of recommendations spread across nine different categories, namely:

- Customer and Community Interests

- Consumer Protection and Advocacy

- Product Features

- Governance

- Regulation and the Law

- Financial Advice

- Underwriting and Claims Management

- Risk Management

By way of example, the Product Features category includes the following recommendations:

- Introduce simpler and cheaper product alternatives

- Develop simpler explanations around what is and is not covered

- Improve communication, understanding and management of risks and uncertainty

- Impose strong controls on level of benefits and income replacement ratios

- Improve Guaranteed Contract Term management

- Embed Loss Minimisation Principle in policy contracts

- Improve data quality

- Improve communication of pricing philosophy

- Improve understanding of Level Premium business

Reference Product and Sustainability Guide

To help address its recommendations, the Taskforce developed a reference product which it says should be used by insurers and their Boards and executives “…to assess risk and uncertainty for both customers and the company.”

In addition to the reference product, the Taskforce also developed a sustainability guide intended to help insurers consider critical aspects of:

- Product design

- Operational practices

- Pricing uncertainty

- Risk management

- Risk appetite

The Taskforce said insurers should use this sustainability guide “…to continually improve their frameworks, policies and day-to-day practices to mitigate risks and improve long term IDII sustainability for consumers and insurers.”

The following links will take advisers and other interested industry colleagues to the Taskforce’s final report, the sustainability guide and the reference product documents:

Findings and Recommended Actions for Individual Disability Income Insurance

Individual Disability Income Insurance Sustainability Guide

Reference Product – Individual Disability Income Insurance

The irony is that the clever diagram at the bottom of the article resembles the top view of a butter churn.

If a car manufacturer sold lemons then they would discontinue the line. The economics is simple. But if a life insurer sells a lemon then they need to keep selling lemons because they have outsourced their distribution model. A financial adviser doesn’t care if the product makes money for the insurer or not – and income protection is a fat premium which equals commission dollars – so they want to keep selling the saleable risk narrative. But if an insurer cans the product – as they should – advisers would flock to whichever insurer still sold the product. That is economics. But insurers keep selling IP out of fear for marketshare and then when the price rises for the loss maker kick in, advisers have a reason to move the product to get that sweet, sweet upfront commission. Again … and again … and again … and …

At what point does the industry consider a future without income protection and it’s trickle down commissions?

Comments are closed.